Scaling Up Private Action for Nature

How Development Finance and Policy Reform Can Close the Global Biodiversity Finance Gap

Biodiversity is no longer just an environmental issue — it has become a core economic and financial stability concern. More than half of global GDP is either moderately or highly dependent on nature and ecosystem services. Agriculture, manufacturing, pharmaceuticals, tourism, fisheries, infrastructure, and even financial markets rely heavily on healthy ecosystems.

Yet despite this dependence, global economic systems continue to accelerate biodiversity loss through deforestation, pollution, unsustainable extraction, and ecosystem degradation. The result is a widening gap between the economic value nature provides and the capital being invested to preserve it.

The OECD’s 2026 report, Scaling Up Private Action for Nature: Opportunities for Development Co-operation and Finance, examines why private capital has not scaled sufficiently toward biodiversity protection and what development institutions, governments, and financial markets must do to change this trajectory.

The report positions biodiversity loss not merely as an ecological challenge, but as a systemic market failure requiring coordinated policy reform, financial innovation, and institutional transformation.

I. The Biodiversity Finance Gap: Why the Current System Is Failing

Nature generates immense economic value, but most ecosystem services remain unpriced. Forests regulate climate, wetlands prevent floods, pollinators support food systems, and oceans sustain livelihoods — yet these services are rarely reflected in market economics.

This creates what economists describe as a “tragedy of the commons,” where natural capital is treated as free and infinitely available.

As a result:

- Ecosystems are overexploited

- Environmental costs are externalized

- Long-term sustainability is sacrificed for short-term economic gains

The OECD report highlights that biodiversity degradation is now creating three major categories of risks for businesses and investors:

1. Physical Risks

Loss of ecosystems directly disrupts supply chains, agricultural productivity, water availability, and climate resilience.

2. Transition Risks

Governments are increasingly introducing stricter environmental regulations, disclosure norms, and sustainability standards that may rapidly alter business models.

3. Liability Risks

Companies may face litigation, penalties, or reputational damage for biodiversity-related harm or non-compliance.

To address this crisis, the Kunming-Montreal Global Biodiversity Framework (KMGBF) establishes ambitious global targets to halt and reverse biodiversity loss by 2030.

Two targets are especially important for the private sector:

Target 15

Businesses must assess, monitor, and disclose nature-related dependencies, risks, and impacts.

Target 19

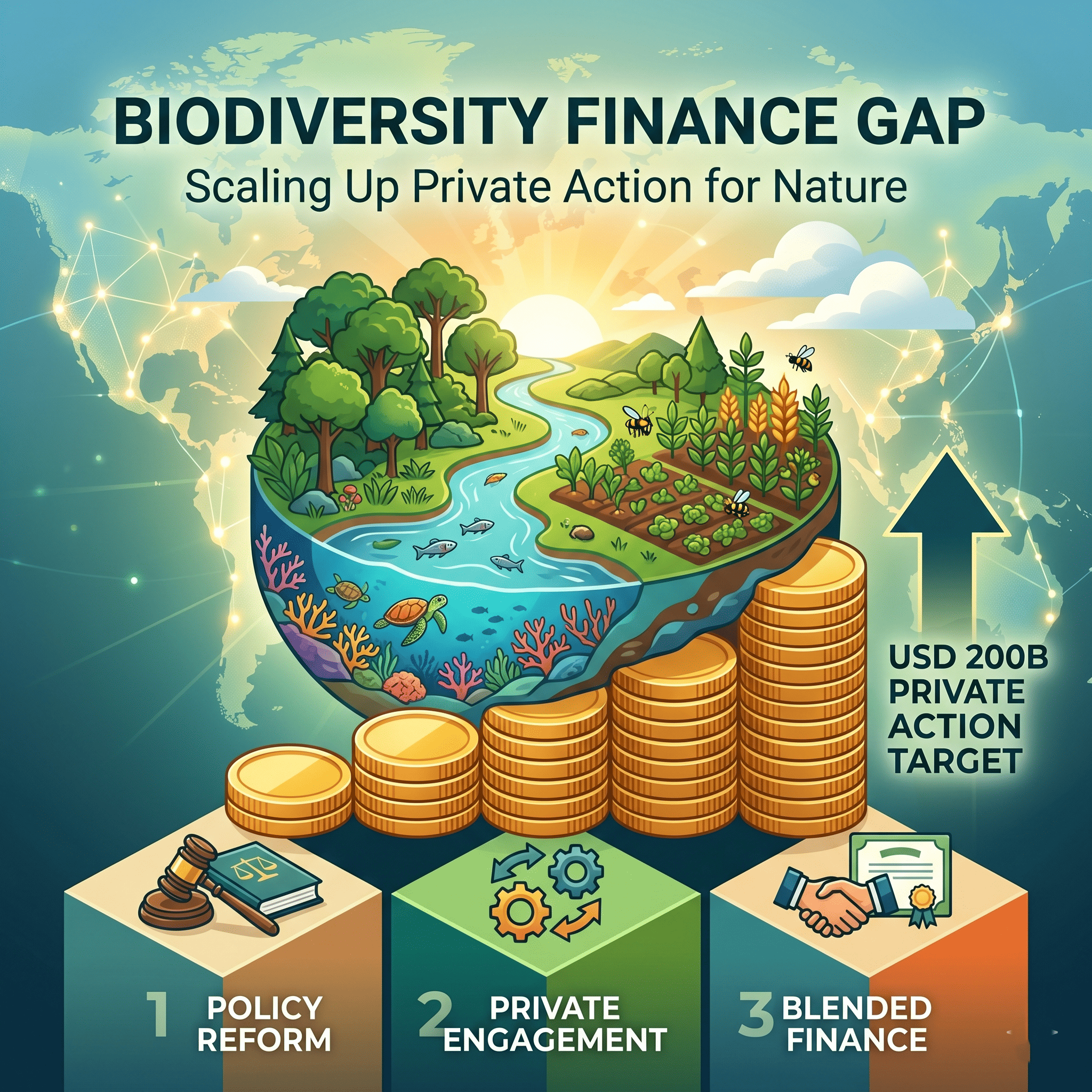

Global biodiversity finance must reach at least USD 200 billion annually by 2030, including substantial mobilization of private capital.

The OECD argues that achieving these targets requires development finance institutions, multilateral banks, and donor agencies to act as “system shapers” rather than merely project financiers.

The report identifies three major strategic pillars for intervention.

II. Pillar One: Strengthening Enabling Environments

Private capital does not flow into nature-positive investments unless policy environments are stable, predictable, and economically viable.

The report emphasizes that governments must first correct structural weaknesses in governance and incentives.

1. Strengthening Property Rights and Resource Governance

One of the biggest barriers to biodiversity investment is unclear ownership and tenure rights.

Investors are unlikely to fund long-term conservation, reforestation, or sustainable agriculture projects if land rights are disputed or poorly documented.

This is particularly relevant in developing economies where customary land ownership systems may lack legal recognition.

The OECD recommends that development institutions support:

- Land registration systems

- Cadastral mapping

- Formalization of customary tenure

- Marine resource governance reforms

Clear property rights reduce investment uncertainty and create a foundation for sustainable economic activity.

2. Reforming Harmful Subsidies and Economic Incentives

Current public subsidy structures often encourage environmentally destructive practices.

For example, agriculture contributes significantly to global deforestation, frequently supported by subsidies promoting land expansion and excessive fertilizer usage.

The report stresses that governments must shift from “nature-negative” incentives toward “nature-positive” economic frameworks.

This includes:

Reforming Harmful Subsidies

Reducing fiscal support for activities that accelerate ecosystem degradation.

Expanding Positive Incentives

Scaling mechanisms such as:

- Payments for Ecosystem Services (PES)

- Watershed protection incentives

- Carbon sequestration payments

- Regenerative agriculture support schemes

Under PES models, landowners or communities receive direct financial compensation for preserving ecosystems and maintaining environmental services.

3. Strengthening National Biodiversity Strategies (NBSAPs)

National Biodiversity Strategies and Action Plans (NBSAPs) are intended to convert global biodiversity commitments into country-level implementation plans.

However, many NBSAPs fail because they remain disconnected from economic ministries, infrastructure planning, and fiscal policy.

The OECD recommends transforming NBSAPs into:

- Costed investment frameworks

- Spatially mapped development strategies

- Clear regulatory roadmaps for investors

This would provide private markets with predictable policy signals and improve investment confidence.

III. Pillar Two: Promoting Private Sector Engagement

Even with better regulations, businesses — particularly in developing economies — face major operational and compliance challenges in transitioning toward nature-positive models.

The report highlights several critical intervention areas.

1. Trade Facilitation and Sustainability Compliance

Global trade is increasingly becoming a driver of biodiversity accountability.

New regulations, such as the European Union Deforestation Regulation (EUDR), require imported commodities like cocoa, timber, coffee, palm oil, and soy to be completely deforestation-free.

While these standards improve sustainability, they also create substantial compliance burdens.

The Major Concern

Micro, Small, and Medium-sized Enterprises (MSMEs), farmers, and cooperatives in developing nations often lack:

- Traceability systems

- Technical expertise

- Certification infrastructure

- Compliance financing

Without support, many risk losing access to international markets.

OECD Recommendation

Development co-operation agencies should provide:

- Technical assistance

- Certification support

- Capacity-building programs

- Sustainability training

- Transition financing

This helps local producers remain competitive in increasingly sustainability-oriented global supply chains.

2. Traceability and Data Infrastructure

Environmental compliance now depends heavily on supply chain transparency.

Companies must increasingly demonstrate where products originate and whether production processes comply with environmental standards.

The report recommends investment in:

- Digital customs systems

- Blockchain-based traceability tools

- Satellite monitoring

- Product tracking technologies

- Environmental verification systems

Robust traceability infrastructure improves market trust and reduces greenwashing risks.

3. Responsible Business Conduct (RBC)

Development institutions can influence corporate behavior through procurement rules, financing conditions, and partnership requirements.

The OECD encourages stronger adoption of:

- Responsible Business Conduct frameworks

- Environmental Impact Assessments (EIAs)

- Biodiversity due diligence standards

This effectively pushes higher environmental standards throughout global supply chains.

IV. Pillar Three: Mobilizing Private Finance for Nature

One of the report’s central findings is that biodiversity projects often struggle to attract commercial investors because they generate uncertain or low financial returns.

As a result, development finance institutions must use blended finance structures and risk-sharing mechanisms to make projects investable.

The report outlines three major financing pathways.

Pathway 1: Direct Investment in Biodiversity Assets

Collective Investment Vehicles (CIVs)

Nature-based projects in developing economies are often:

- Small-scale

- Fragmented

- Operationally complex

Large institutional investors typically avoid such projects due to high transaction costs.

Collective Investment Vehicles solve this by pooling multiple projects into larger investment portfolios.

Development banks can provide “first-loss” capital through junior equity tranches, absorbing initial risks and making the investment structure more attractive for private investors participating through senior debt tranches.

This blended finance approach significantly improves risk-adjusted returns.

Biodiversity and Blue Bonds

The report highlights the rapid growth of thematic bond markets.

These include:

- Green Bonds

- Sustainability Bonds

- Blue Bonds

- Biodiversity Bonds

Such instruments allow issuers to raise capital specifically for environmental initiatives.

A notable example is BBVA Colombia’s biodiversity bond, supported by the IFC, which finances:

- Reforestation

- Regenerative agriculture

- Ecosystem restoration

These instruments help channel institutional capital toward nature-positive activities.

Pathway 2: Integrating Biodiversity into Broader Sustainable Finance

Sustainability-Linked Bonds (SLBs)

Unlike Green Bonds, SLBs do not restrict how proceeds are used.

Instead, financing costs are linked to sustainability performance indicators.

For example:

- Failure to meet biodiversity targets may increase borrowing costs

- Achievement of targets may reduce coupon obligations

Chile issued the world’s first sovereign SLB linked to biodiversity KPIs tied to expanding protected areas.

This represents a significant evolution in sovereign sustainability financing.

Debt-for-Nature Swaps

Debt-for-nature swaps are particularly important for heavily indebted developing economies.

Under these arrangements:

- Existing sovereign debt is refinanced or restructured

- Development banks provide guarantees

- Debt servicing costs decline

- Financial savings are redirected into domestic conservation initiatives

Recent transactions in Caribbean nations and El Salvador demonstrate growing momentum for these structures.

Tropical Forest Forever Facility (TFFF)

The OECD also discusses the Tropical Forest Forever Facility launched at COP30.

This large-scale blended finance mechanism aims to:

- Attract commercial capital into green bond portfolios

- Use investment returns to compensate investors

- Redirect part of the returns as grants to countries successfully preserving tropical forests

The structure attempts to create long-term financial incentives for conservation at sovereign scale.

Pathway 3: Leveraging Existing Carbon Markets

Rather than waiting for biodiversity credit markets to mature, the report recommends integrating biodiversity benefits into existing carbon finance mechanisms.

Outcome Bonds

One major example is the World Bank’s Amazon Outcome Bond.

The structure works as follows:

- Investors accept lower fixed returns

- The forgone interest finances reforestation projects

- Projects generate verified Carbon Removal Units (CRUs)

- Corporate buyers such as Microsoft pre-purchase these CRUs

- Successful project outcomes generate variable investor returns

This creates a direct link between ecological performance and financial reward.

V. Operational Bottlenecks Limiting Scale

Despite growing innovation, the OECD identifies several structural barriers preventing rapid scaling of biodiversity finance.

1. Financial and Structural Complexity

Blended finance structures, sovereign debt swaps, and outcome-based instruments are highly complex.

They require:

- Extensive legal structuring

- Multi-party negotiations

- Long implementation timelines

- Significant transaction costs

This limits scalability and replication.

2. The “Bankability” Problem

There remains a severe shortage of investable biodiversity projects with:

- Predictable revenue models

- Clear cash flows

- Strong governance structures

Many projects remain dependent on grants and struggle to transition toward commercial viability.

3. Data Fragmentation and Greenwashing Risks

The absence of a universally accepted taxonomy for “nature-positive” investments creates confusion across markets.

Multiple ESG frameworks increase reporting burdens and reduce comparability.

Additionally, measuring:

- Additionality

- Permanence

- Ecological impact

remains technically difficult, increasing the risk of greenwashing.

4. Institutional Capacity Constraints

Many development institutions still lack dedicated biodiversity expertise.

Nature-related investments are often treated as secondary co-benefits within climate programs rather than standalone strategic priorities.

This slows:

- Deal structuring

- Procurement

- Project evaluation

- Market development

Conclusion

The OECD’s report makes one point exceptionally clear: biodiversity protection can no longer rely solely on public funding or philanthropic initiatives.

The scale of the crisis demands systemic private sector participation.

However, private capital will only mobilize at scale when governments, development institutions, and financial markets collectively address the structural barriers preventing investment.

This requires:

- Policy certainty

- Strong governance

- Economic incentive reform

- Robust traceability systems

- Innovative blended finance mechanisms

- Standardized biodiversity metrics

The transition toward a nature-positive economy is ultimately not just an environmental necessity — it is becoming a core requirement for long-term economic resilience, financial stability, and sustainable global development.

Comments

No Comments yet