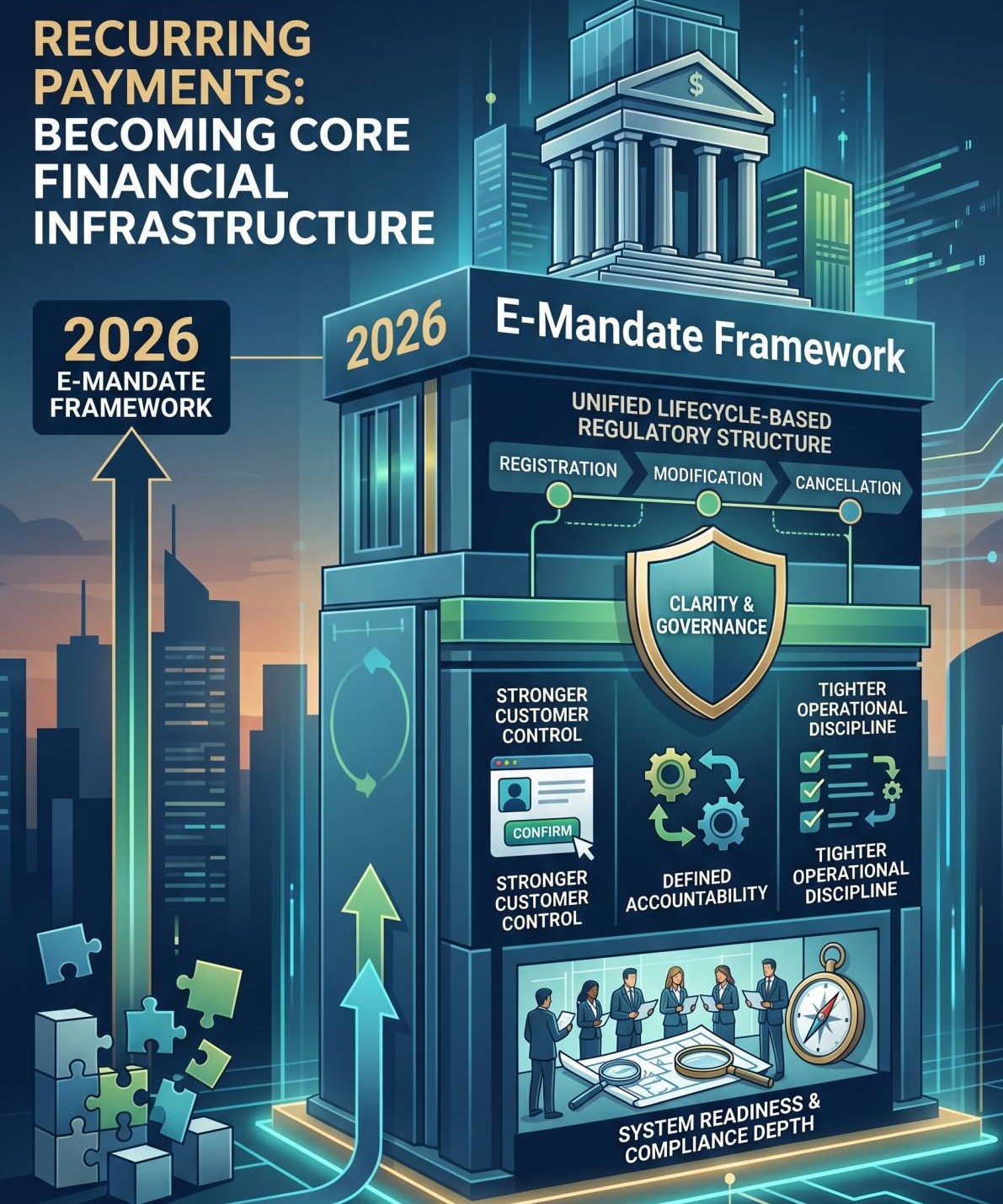

A Consolidation That Signals Maturity in Digital Payments

The Reserve Bank of India has introduced the Digital Payments – E-Mandate Framework, 2026, replacing a series of fragmented circulars issued between 2019 and 2024.

At first glance, this may appear as a routine consolidation. But a closer reading shows that the RBI has not merely compiled existing rules—it has refined, clarified, and strengthened operational aspects of recurring digital payments across cards, UPI, and PPIs.

This marks a shift from a reactive regulatory approach to a structured, system-driven framework.

What Has Actually Changed?

1. Formal Consolidation with Legal Backing

Earlier guidelines were scattered across multiple circulars.

Now, all provisions are unified under a single legally enforceable direction issued under the PSS Act, 2007.

What changes:

- One authoritative framework replaces 8 earlier circulars

- Improves regulatory clarity and enforceability

2. Mandatory AFA for Full Lifecycle (Not Just Registration)

Previously, AFA (Additional Factor Authentication) was primarily emphasized at registration and select transactions.

Now clarified and expanded:

- AFA is mandatory for:

- Registration of e-mandate

- First transaction

- Any modification or revocation

- Opt-out requests

Impact:

Authentication is now embedded across the entire mandate lifecycle, not just entry points.

3. Clearer Customer Control Over E-Mandates

The new framework strengthens user autonomy.

New / clarified requirements:

- Mandatory specification of validity period

- Facility to:

- Modify mandate validity anytime

- Withdraw mandate anytime

- For variable mandates:

- Customers can set maximum transaction cap

Impact:

Shifts control structurally toward the customer—not just operationally.

4. Pre-Transaction Notification: More Structured + Explicit

While pre-debit alerts existed earlier, the framework now standardizes their content and intent.

What’s tightened:

- Mandatory notification at least 24 hours before debit

- Must include:

- Merchant name

- Exact amount

- Date/time

- Mandate reference

- Reason for debit

- Explicit opt-out mechanism with AFA validation

Exception introduced clearly:

- No pre-notification required for:

- FASTag auto-replenishment

- NCMC transactions

Impact:

From “intimation” → actionable customer intervention window

5. Transaction Limits Rationalized and Expanded

This is one of the most practical changes.

Revised clarity:

- Up to Rs15,000 → No AFA required

- Above Rs15,000 → AFA mandatory

Special category enhancement:

- Up to Rs1,00,000 without AFA for:

- Insurance premiums

- Mutual fund subscriptions

- Credit card bill payments

Impact:

Balances customer convenience with risk control, especially for financial commitments.

6. Post-Transaction Transparency Strengthened

Earlier post-debit alerts lacked uniform depth.

Now required to include:

- Transaction details

- Mandate reference

- Reason for debit

- Grievance redressal details (new addition)

Impact:

Improves audit trail and dispute defensibility.

7. Explicit Zero-Cost Mandate for Customers

A critical consumer-centric clarification.

Now clearly stated:

- No charges can be levied for using e-mandate facility

Impact:

Removes hidden friction in recurring payment adoption.

8. Card Reissuance Continuity Introduced

A practical operational gap is now addressed.

New provision:

- Existing e-mandates can be mapped to reissued cards

Impact:

Reduces mandate failures due to card replacement—important for subscription economy.

9. Stronger Accountability on Ecosystem Participants

Responsibility is now more explicitly distributed.

Clarified roles:

- Issuers → Customer interface, authentication, alerts

- Acquirers → Ensure merchant compliance

Impact:

Shifts from shared ambiguity → defined accountability architecture

Why This Matters

1. Recurring Payments Are Becoming Infrastructure

Subscriptions, SIPs, insurance, SaaS—recurring payments are no longer optional—they are financial infrastructure.

This framework ensures that infrastructure is:

- Predictable

- Auditable

- Customer-controlled

2. Reduced Regulatory Ambiguity for Businesses

Earlier, multiple circulars created interpretation gaps.

Now:

- A single framework = lower compliance friction

- Easier implementation for fintechs, banks, and platforms

3. Stronger Consumer Protection Without Killing Convenience

The RBI avoids over-regulation by:

- Allowing high-value exemptions (Rs1 lakh cases)

- Maintaining AFA only where risk justifies it

This is precision regulation, not blanket control.

Practical Implications for Professionals

For CAs / Auditors

- Review e-mandate controls and documentation

- Validate:

- AFA logs

- Notification systems

- Opt-out trails

- Increased relevance in system audits and payment compliance reviews

For Compliance Teams

- Update SOPs for:

- Mandate lifecycle management

- Customer communication protocols

- Ensure merchant agreements reflect new obligations

For Fintechs / Payment Companies

- Reconfigure:

- Notification engines

- Risk controls (velocity + thresholds)

- Opportunity to optimize customer experience within compliance boundaries

For Businesses Using Auto-Debit Models

- Subscription models become more stable

- Reduced payment failures due to:

- Card reissuance mapping

- Clear mandate controls

Closing Insight

This framework is not introducing disruption—it is eliminating ambiguity.

The real shift is subtle but significant:

From rules scattered across circulars → a coherent, lifecycle-based regulatory architecture

For professionals, the takeaway is clear:

This is less about reacting to change—and more about tightening systems before scrutiny does it for you.

Comments

No Comments yet