The Pension Fund Regulatory and Development Authority (PFRDA) has introduced a significant enhancement to the National Pension System (NPS) framework through its circular dated May 15, 2026, by launching Retirement Income Schemes (RIS) and new Drawdown Options for subscribers.

The initiative is aimed at strengthening post-retirement financial planning by providing subscribers with greater flexibility, structured periodic payouts, and continued investment participation during the decumulation phase — the stage after retirement when accumulated pension wealth begins to be withdrawn.

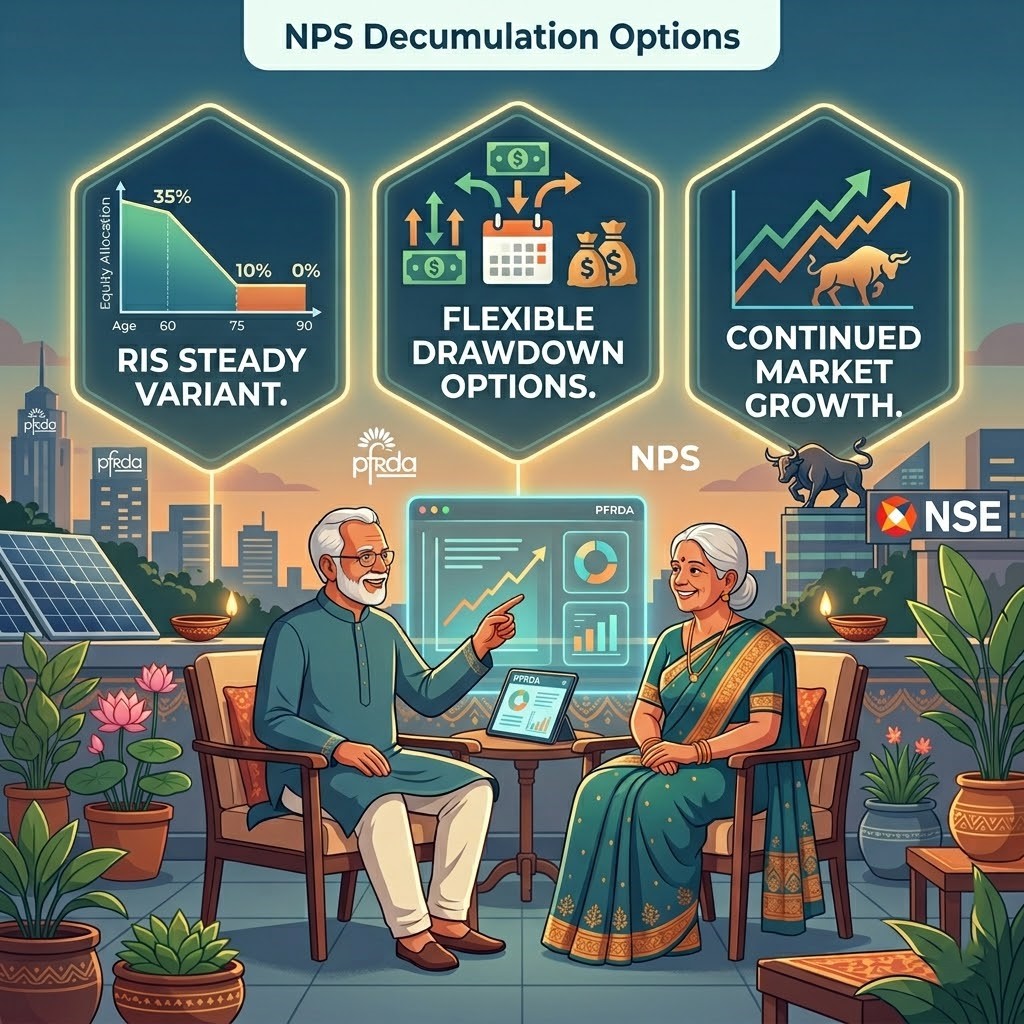

Introduction of Retirement Income Schemes (RIS)

As part of the revised framework, PFRDA has introduced the RIS Steady Variant, designed to help retirees manage longevity risk while allowing the remaining pension corpus to continue participating in market-linked growth opportunities.

Glide Path-Based Asset Allocation

The RIS framework follows a glide path approach, under which the allocation to equity gradually reduces with age in order to balance growth potential and risk management.

The proposed allocation structure is as follows:

- Equity exposure begins at 35% at age 60

- It gradually reduces over time

- Equity allocation reaches 10% by age 75

- The 10% exposure continues until age 85

This mechanism is intended to create a progressively conservative investment profile as subscribers advance in age.

Introduction of Flexible Drawdown Options

The circular also introduces multiple payout mechanisms for subscribers opting to receive periodic withdrawals from the lump sum component of their NPS corpus upon exit.

Importantly, these provisions do not alter the mandatory annuity purchase requirements applicable under NPS regulations.

Subscribers may now choose between the following payout methods:

1. Systematic Payout Rate (SPR) – Default Option

Under SPR:

- Payout amounts are determined based on a variable withdrawal rate

- The payout amount is recalculated annually

- Calculations are based on the prevailing market value of the remaining corpus

This approach allows payouts to dynamically adjust in line with investment performance and residual corpus levels.

2. Systematic Unit Redemption (SUR)

Under SUR:

- Subscribers can opt for redemption of units in equal installments

- The withdrawal schedule is spread across the chosen payout period

This option provides a more structured and predictable withdrawal pattern.

Key Features of the Revised Framework

Eligibility

The framework is applicable to:

- Government sector NPS subscribers

- Non-Government sector NPS subscribers

Payout Duration

Periodic payouts may continue up to:

- 85 years of age

Payout Frequency Options

Subscribers may select:

- Monthly payouts

- Quarterly payouts

- Annual payouts

based on individual financial requirements.

Continued Investment Flexibility

Subscribers can:

- Continue with their existing Pension Fund Manager (PFM)

- Switch pension funds once every two financial years

This allows continued investment management flexibility even during retirement.

Protection in Case of Death

In the event of the subscriber’s demise during the payout phase:

- The remaining corpus shall be distributed in accordance with the PFRDA (Exits and Withdrawals) Regulations, 2015.

Important Considerations for Subscribers

Market-Linked Nature of Returns

PFRDA has clarified that:

- The payout mechanism is market-linked

- No guaranteed return or assured payout amount is provided

Accordingly, actual payouts and corpus value will remain subject to market performance and investment risks.

Enhanced Transparency Measures

To improve subscriber awareness and decision-making:

- Pension Funds and Central Record Keeping Agencies (CRAs) will be required to provide detailed disclosures

- Online calculators and simulators must be made available to help subscribers estimate:

- Expected payouts

- Residual corpus values

- Potential investment outcomes

Annual Retirement Income Statement

Subscribers will receive a dedicated:

Retirement Income Statement

on their birthday each year.

The statement will include:

- Revised payout details (for SPR subscribers)

- Asset allocation changes

- Corpus balance information

- Rebalancing summary

Residual Corpus at End of Drawdown Period

At the conclusion of the selected drawdown tenure, any remaining corpus may be:

- Withdrawn as a lump sum, or

- Utilised for annuity purchase

depending on subscriber preference and regulatory provisions.

Regulatory Significance and Practical Impact

The introduction of RIS and flexible drawdown mechanisms represents a notable evolution in India’s pension ecosystem.

Traditionally, post-retirement options under pension systems have focused primarily on:

- Lump sum withdrawal, or

- Fixed annuity structures

The revised framework attempts to create a more flexible and investment-oriented retirement income model by:

- Extending investment participation after retirement

- Allowing customisable payout frequencies

- Providing adaptive withdrawal mechanisms

- Balancing growth potential with age-based risk reduction

For retirees, this may enhance:

- Liquidity management

- Financial planning flexibility

- Long-term corpus sustainability

For pension administrators and intermediaries, the framework will require:

- Operational system upgrades

- Enhanced disclosure mechanisms

- Improved investor education initiatives

- Robust communication frameworks

Conclusion

PFRDA’s introduction of Retirement Income Schemes (RIS) and flexible drawdown options marks a significant step toward modernising post-retirement income management under the National Pension System.

The framework provides subscribers with:

- Greater flexibility in accessing retirement savings

- Continued market participation

- Structured payout options

- Enhanced transparency and disclosure mechanisms

While the market-linked nature of the scheme requires careful financial planning and risk assessment, the initiative represents a progressive shift toward more dynamic and personalised retirement income solutions in India’s pension landscape.

Note: The framework will become operational from a date to be separately notified by PFRDA upon completion of the required technological and operational implementation arrangements.

Comments

No Comments yet