In a profession where technical competence is almost a given, what truly separates a reliable Chartered Accountant from a trusted one is not intelligence—it’s discipline. Not the motivational kind, but the operational kind. The kind that shows up in routines, decisions, documentation, and accountability—especially when no one is watching and pressure is high.

Over time, one pattern becomes evident across high-performing professionals and firms: excellence is not episodic, it is systematic. And at the core of that system lies disciplined behaviour.

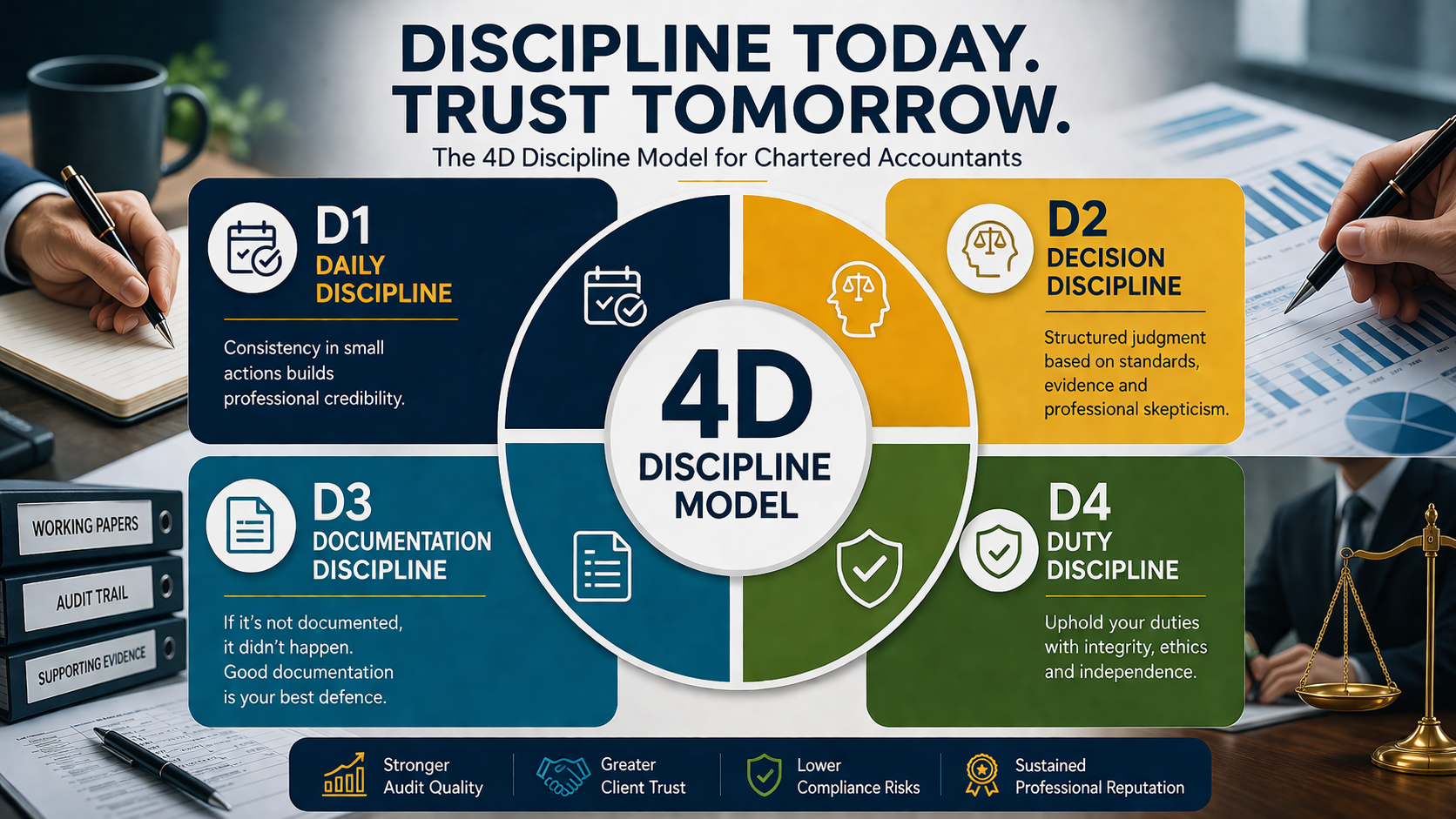

To translate this into something practical and implementable, consider the 4D Discipline Model for Chartered Accountants—a framework that converts discipline from an abstract ideal into a structured professional capability.

D1 – Daily Discipline

Consistency is the foundation of credibility.

Daily discipline is about showing up prepared, meeting timelines, reviewing work with rigor, and maintaining professional hygiene in even the smallest tasks. Whether it’s clearing emails, updating working papers, or following up with clients—these micro-actions compound into macro-reputation.

Why it matters:

In audit and compliance, delays and oversights rarely arise from lack of knowledge—they stem from broken routines. Daily discipline ensures execution reliability.

D2 – Decision Discipline

Good judgment is not instinctive—it is structured.

Every CA makes dozens of decisions daily—materiality thresholds, audit procedures, interpretations, client positions. Decision discipline means anchoring these choices in standards, evidence, and professional skepticism rather than convenience or pressure.

Why it matters:

Regulatory scrutiny doesn’t evaluate effort—it evaluates decisions. A disciplined decision-making approach protects both professional standing and firm reputation.

D3 – Documentation Discipline

If it’s not documented, it didn’t happen.

From an audit and compliance lens, documentation is not clerical work—it is legal defence. Proper working papers, audit trails, and contemporaneous records are what stand between a professional and potential litigation or regulatory action.

Why it matters:

Standards like SA 230 (Audit Documentation) exist for a reason. Weak documentation is one of the most common gaps observed in peer reviews and inspections.

D4 – Duty Discipline

Integrity is demonstrated through action, not intent.

Duty discipline is about honoring professional responsibilities—maintaining independence, managing conflicts of interest, upholding confidentiality, and prioritizing ethical obligations over commercial pressures.

Why it matters:

In a trust-based profession, ethical lapses are far more damaging than technical errors. Duty discipline ensures long-term credibility over short-term gains.

The Larger Shift: From Skill to System

What makes this model relevant is not its simplicity—but its applicability.

Most professionals focus heavily on upgrading technical knowledge, but sustainable excellence comes from embedding disciplined systems into daily practice. Firms that institutionalize such behavioural frameworks often see stronger audit quality, better client trust, and lower compliance risks.

Closing Thought

Discipline in the CA profession is not about rigidity—it’s about reliability.

And in an environment where scrutiny is increasing and stakeholder expectations are evolving, discipline is no longer optional—it is a competitive advantage.

The question is not whether discipline matters.

The real question is: Is it structured enough to be repeatable

Comments

No Comments yet